The first thing that stands out about this company is how quietly and deliberately it has evolved from a narrow technology platform into a fully integrated commercial biopharmaceutical organization focused on solving difficult problems in chronic disease care. What began as a formulation science company has gradually transformed into a specialty pharmaceutical business with proprietary delivery platforms, regulatory approvals, commercial infrastructure, and a growing presence in highly specialized therapeutic areas. The company’s roots are not in chasing blockbuster drugs or headline-driven innovation, but in building enabling technologies that solve practical pharmaceutical challenges such as drug stability, delivery, and patient usability, especially in indications where conventional formulations fail to meet clinical needs.

Xeris Biopharma (NASDAQ:XERS) was founded on the premise that many highly effective molecules never reach their full clinical or commercial potential because they cannot be formulated, stored, or delivered in a way that is convenient or reliable for patients and healthcare providers. From its earliest days, the company focused on developing novel formulation technologies capable of stabilizing complex molecules in ready-to-use liquid form, eliminating the need for reconstitution, refrigeration, or complex preparation steps. This scientific foundation led to the development of the company’s proprietary formulation platforms, which became the cornerstone of its identity and long-term strategy in pharmaceutical development and commercialization.

As the company matured, Xeris Biopharma Holdings, Inc. expanded beyond formulation science into full-scale drug development, regulatory execution, and commercial operations. This shift marked a defining moment in the company’s evolution, transforming it from a platform-centric research organization into a commercial-stage biopharmaceutical company with an integrated value chain spanning research and development, manufacturing, regulatory affairs, marketing, and distribution. This vertical integration allowed the company to retain control over product development timelines, clinical strategy, regulatory positioning, and commercial launch execution, reducing dependence on partners and increasing long-term value capture.

The company strategically positioned itself within the pharmaceutical landscape by targeting chronic endocrine and neurological diseases that affect relatively small but medically complex patient populations. These conditions often lack sufficient therapeutic options and require specialized treatments that are unattractive to large pharmaceutical companies focused on mass-market scale. By focusing on these underserved niches, Xeris Biopharma Holdings, Inc. established a differentiated commercial model that emphasizes depth over breadth, prioritizing specialized physician relationships, payer engagement, and patient support rather than high-volume marketing campaigns. This approach enabled the company to build durable franchises in markets where clinical expertise and product reliability matter more than brand visibility.

Over time, Xeris Biopharma Holdings, Inc. built its reputation around its ability to bring difficult-to-formulate drugs to market in stable, patient-friendly formats. This capability not only supported its initial product launches but also became a repeatable innovation engine that could be applied to new molecules, new indications, and lifecycle extensions of existing therapies. The company’s formulation platforms evolved from being purely technical tools into strategic assets that shape product differentiation, regulatory positioning, and commercial competitiveness. This transformation elevated the company’s role from being a supplier of formulation technology to being a creator and owner of pharmaceutical products with long-term commercial value.

The geographic and operational footprint of Xeris Biopharma Holdings, Inc. reflects its commitment to maintaining close control over its development and commercialization processes. With operations centered in the United States, the company developed regulatory expertise aligned with FDA standards, manufacturing partnerships capable of meeting pharmaceutical quality requirements, and commercial teams focused on specialized physician networks. This infrastructure allowed the company to move efficiently from clinical development into commercialization without relying heavily on external licensing or co-promotion agreements, preserving strategic flexibility and economic upside.

As the company expanded its commercial presence, it also developed internal capabilities in market access, payer negotiations, and patient services, recognizing that in chronic disease markets, reimbursement, adherence, and patient experience are as critical as clinical efficacy. This focus on the full ecosystem surrounding pharmaceutical products became a defining feature of the company’s operating philosophy. Rather than treating commercialization as a downstream function, Xeris Biopharma Holdings, Inc. integrated commercial considerations into its development strategy from the earliest stages, ensuring that new products are designed not only to meet clinical needs but also to fit within real-world healthcare systems.

The evolution of Xeris Biopharma Holdings, Inc. mirrors a broader shift within the biotechnology sector, where the most successful companies are no longer those that merely invent new molecules, but those that can transform scientific innovation into sustainable, profitable businesses. By prioritizing operational discipline, financial prudence, and focused execution, the company gradually repositioned itself from a speculative biotech profile into a specialty pharmaceutical identity characterized by recurring revenue, growing cash flow, and increasing predictability. This transformation was not driven by a single breakthrough, but by a sequence of deliberate strategic choices that emphasized platform development, niche market focus, and long-term value creation.

Today, Xeris Biopharma Holdings, Inc. stands as an example of how a biopharmaceutical company can evolve from a technology-driven startup into a commercial organization with durable competitive advantages. Its background is defined not by hype cycles or speculative trends, but by a steady accumulation of scientific capability, regulatory expertise, and commercial infrastructure. This history explains why the company is increasingly viewed not as a risky development-stage biotech, but as a growing specialty pharmaceutical company positioned for long-term relevance within its chosen therapeutic domains.

A commercial-stage biotech quietly transforming into a cash-compounding specialty pharma platform

Xeris Biopharma Holdings, Inc. is increasingly being recognized not as a speculative clinical-stage biotech, but as a commercial-stage biopharmaceutical company that is methodically transitioning into a profitable, cash-generating specialty pharma platform. Headquartered in Illinois, Xeris develops and commercializes therapies focused on chronic endocrine and neurological diseases, targeting highly specialized patient populations that are underserved by large pharmaceutical companies. This strategic focus on complex niche markets gives Xeris pricing power, durable payer relationships, and regulatory protection, while insulating the company from the intense competition and commoditization seen in broader therapeutic categories.

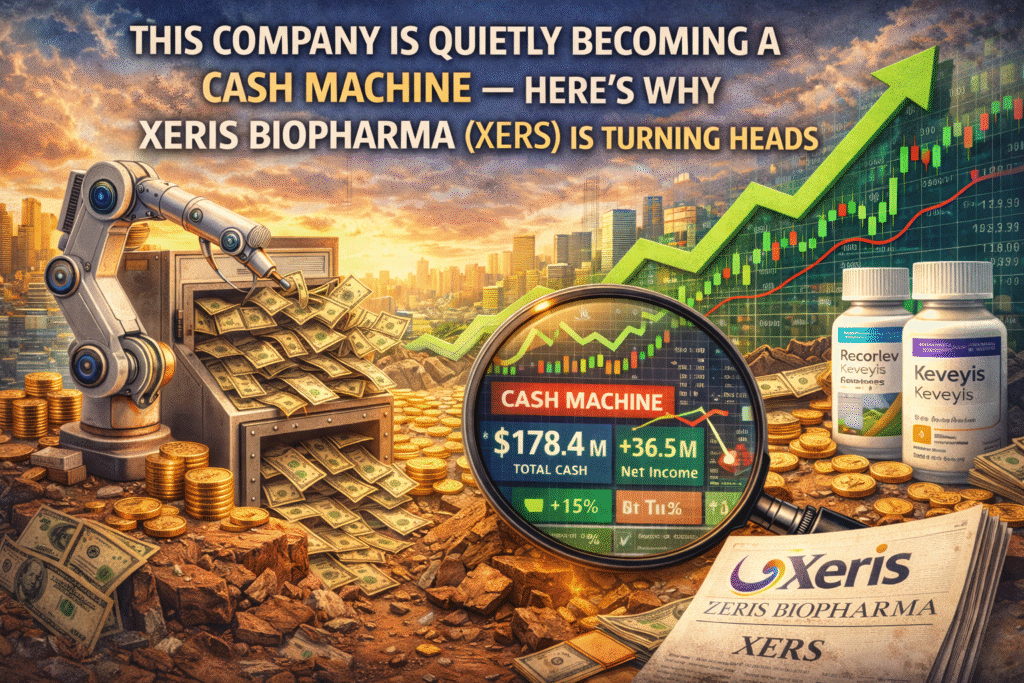

As of mid-December, Xeris Biopharma Holdings, Inc. was trading at approximately $7.05 per share, with a forward P/E ratio near 64 according to Yahoo Finance. On the surface, this valuation can appear expensive. However, this metric does not capture the inflection Xeris is undergoing. The company is moving from survival-stage biotech to profitable specialty pharma, supported by three marketed products and a pipeline that is approaching its next major value creation phase. Revenue is projected to surpass $360 million by 2026, driven primarily by the continued expansion of Recorlev and the advancement of XP-8121. Longer-term models suggest revenue could exceed $900 million by 2028 with EBITDA margins of 22 to 25 percent, translating into roughly $240 million in EBITDA.

Despite this growth trajectory, Xeris trades at approximately 11x forward EBITDA, compared to 12x to 14x for comparable specialty pharma peers. This disconnect creates a valuation re-rating opportunity as the market recognizes the company’s improving profitability, growing cash flows, and reduced business risk.

CHECK THIS OUT: Corcept (CORT) Skyrockets 1,534% in 10 Years and Immuneering (IMRX) Reports 86% 9-Month Survival in Pancreatic Cancer.

The structural shift from biotech risk to specialty pharma cash flow

Most biotechnology companies are valued as binary science experiments, where outcomes depend on clinical trial success and regulatory approvals. Xeris has already passed that stage. It operates as a commercial-stage biopharmaceutical company with three marketed products generating recurring revenue and funding future growth internally. This is a critical transformation because it changes how the business is valued, financed, and perceived by institutional investors.

Xeris’ transition is underpinned by a self-reinforcing financial flywheel. Free cash flow is used to reduce debt, which lowers balance sheet risk and improves investor confidence. Improved confidence attracts institutional capital, reducing the company’s cost of equity and allowing valuation multiples to expand faster than earnings growth alone would justify. This creates a compounding effect where cash flow, risk perception, and valuation all reinforce each other.

Importantly, capital allocation at Xeris is conservative and disciplined. Management prioritizes organic growth, internal funding for pipeline development, and debt reduction rather than pursuing aggressive acquisitions or dilutive expansions. This restraint preserves shareholder value and allows the company to maintain focus on its core competencies.

Proprietary formulation platforms as a defensible competitive moat

One of the most underappreciated strengths of Xeris Biopharma is its proprietary formulation technology. The company’s XeriSol and XeriJect platforms allow it to create stable liquid formulations of drugs that are otherwise difficult to formulate, store, or administer. This capability is not easily replicated, and it provides a meaningful barrier to entry.

These platforms do not merely support existing products. They also create optionality for pipeline expansion and lifecycle management. By applying these formulation technologies to new molecules, Xeris can improve patient convenience, enhance drug stability, and differentiate its products in crowded therapeutic spaces. This creates regulatory exclusivity, intellectual property protection, and commercial defensibility that together form a durable moat.

Recorlev, one of Xeris’ flagship products, benefits from both regulatory protection and formulation advantages that make it difficult for competitors to displace. XP-8121, currently advancing through development, could become another cornerstone product leveraging the same technological strengths.

Focused market strategy in high-complexity niches

Xeris deliberately targets small, complex, and underserved markets that are unattractive to large pharmaceutical companies. This is a strategic advantage. Large pharmaceutical firms prioritize massive addressable markets with broad patient populations. Xeris instead focuses on areas where patient needs are high, clinical complexity is significant, and competition is limited.

This niche-focused commercial model allows Xeris to build deep relationships with physicians, payers, and patient advocacy groups. It enables premium pricing, stable reimbursement, and predictable demand. Rather than chasing scale, Xeris prioritizes operational precision, ensuring that each product achieves high penetration within its specific market.

This strategy reduces competitive intensity, improves gross margins, and supports long-term profitability, all while minimizing marketing inefficiencies and commercial risk.

Valuation asymmetry and upside potential

At current valuation levels, the market is still pricing Xeris as a risky biotech rather than as a growing specialty pharma company. This creates an asymmetrical opportunity for investors. A base-case scenario using a 12x multiple on projected 2030 EBITDA implies a share price in the range of $17 to $18. A bull case, where revenue growth accelerates and margins expand more rapidly, supports valuation estimates in the $25 to $28 range. A bear case suggests downside is limited near current levels because the company already generates recurring cash flow and carries a relatively low-risk balance sheet.

This asymmetric profile, where downside is buffered by cash flow and upside is driven by growth and multiple expansion, is particularly attractive in volatile markets.

Risk profile and mitigation

The risks associated with Xeris are operational rather than existential. They include execution risk, payer adoption timing, cash flow variability, and market sentiment shifts. These risks are mitigated by Xeris’ specialized commercialization approach, disciplined financial management, and track record of consistent delivery.

Unlike early-stage biotechs, Xeris does not face the risk of catastrophic failure from a single clinical trial. Its diversified product base and growing cash flows provide resilience and stability.

Comparison with other specialty pharma success stories

A useful comparison is Harrow, Inc., which has also demonstrated how a focused specialty pharma model can deliver strong returns through operational execution and disciplined capital allocation. Harrow’s stock appreciated following similar profitability transitions and market recognition. Xeris shares many of the same structural characteristics but remains earlier in its valuation re-rating process.

Hedge fund interest and institutional perception

Xeris Biopharma Holdings, Inc. is not currently among the most popular hedge fund stocks, with approximately 30 hedge funds holding positions as of the third quarter. This relative lack of crowded institutional ownership suggests that the opportunity remains under-discovered, providing room for future demand as the company continues to hit financial milestones.

While some investors may prefer AI-focused equities for near-term momentum, Xeris offers a fundamentally driven, cash-flow-based compounding story that can deliver attractive long-term returns through disciplined growth, margin expansion, and valuation normalization.

Final perspective on Xeris Biopharma Holdings, Inc.

Xeris is not a hype-driven biotech story. It is a methodical transformation from a development-stage company into a profitable specialty pharmaceutical business with a defensible moat, recurring revenue, and strong capital discipline. Its proprietary platforms, niche market focus, and financial flywheel create a rare combination of growth and stability.

For investors seeking exposure to healthcare with less binary risk and more operational leverage, Xeris Biopharma Holdings, Inc. represents a compelling long-term opportunity positioned for compounding value creation as profitability, scale, and market recognition converge.

READ ALSO: Tiziana (TLSA) Surges 143% in 2025 and Immuneering (IMRX) Reports 86% 9-Month Survival in Pancreatic Cancer.