We recently published our article Top 5 Best Biotech Micro-Caps With Major Clinical Catalysts in 2026. This piece looks at Mind Medicine (MindMed) Inc. (NASDAQ: MNMD) as biotech sentiment firms on renewed risk appetite, a packed 2026 clinical trial calendar, and rising demand for differentiated mental health therapies that can deliver clearer, faster outcomes in real-world psychiatry.

Biotechnology is one of the few sectors where a single new dataset can instantly rewrite a company’s story, because drug development is built around proof—proof of efficacy, proof of safety, and proof that regulators will allow a therapy to move from clinical promise to commercial reality. That’s why biotech investing behaves differently from most software or industrial stocks. Instead of steady quarterly demand signals, clinical-stage biotech stocks often trade around clinical trial milestones like Phase 2 results, Phase 3 topline data, and FDA decision dates, where outcomes can be binary and price moves can be violent. In 2026, the calendar is packed with the kind of clinical readouts and regulatory catalysts that typically pull micro-cap biotech stocks back into the spotlight, especially when valuations are still recovering from prior risk-off cycles and investors are hunting for asymmetric upside.

Why Micro-Cap Biotech Is the “Asymmetric Upside” Corner of Healthcare

Biotech micro-caps—often defined as small-cap to micro-cap biotech stocks under roughly $5 billion in market cap—sit in a high-volatility sweet spot. These companies are usually earlier in the drug development curve, with fewer commercial products (or none at all), and their valuation is heavily tied to one or two lead programs. That concentration is exactly what creates “major clinical catalysts.” When a micro-cap biotech company reports a clean Phase 2 signal that supports dose, mechanism, and patient benefit, it can unlock larger Phase 3 designs, partnerships, or even acquisition interest. When Phase 3 data lands, it can flip the market from “probability discount” to “commercial modeling,” which is where multiples and market caps can expand rapidly.

In 2026, that asymmetry matters because the market tends to reward clarity. Investors can tolerate risk; they struggle with uncertainty. A biotech pipeline with defined endpoints, known timelines, and a credible regulatory pathway is often treated as higher quality than a vague “platform story” with distant payoffs. This is why phrases like “clinical catalyst,” “topline data,” “pivotal trial,” “PDUFA date,” “NDA submission,” and “FDA approval” become the SEO backbone of biotech watchlists: they reflect the real triggers that reprice biotech stocks.

The “Catalyst Cycle”: How Biotech Stocks Typically Reprice Around Data and FDA Milestones

The biotech catalyst cycle tends to follow a familiar pattern. First comes anticipation, when traders and long-term holders position ahead of an expected clinical trial update. Then comes the data event: a press release, a medical conference presentation, or a regulatory decision. Finally comes the reassessment phase, when analysts and investors re-estimate probability of success, addressable market, pricing power, competitive positioning, and time to commercialization. Micro-cap biotech stocks can swing the most because expectations are often fragile, liquidity is thinner, and there’s less “institutional dampening” compared to mega-cap pharma.

What makes 2026 especially relevant is that it’s not just about one type of catalyst. It’s a year where many clinical-stage biotech companies are stacked across multiple inflection points: mid-stage Phase 2 readouts that determine whether a program earns the right to be pivotal, late-stage Phase 3 readouts that can support FDA filings, and regulatory outcomes that can instantly transform revenue expectations. For investors, this means the opportunity isn’t only “pick the best science.” It’s also “pick the best timing,” because catalyst density can create multiple chances for sentiment to flip.

Where the Biggest 2026 Biotech Catalysts Are Concentrated

Clinical catalysts in 2026 are likely to cluster in therapeutic areas where unmet need is obvious and regulators have clear frameworks: oncology, rare disease, immunology/inflammation, neurology and mental health, and select cardiometabolic or specialty indications. Oncology remains a catalyst engine because endpoints and biomarker strategies can produce meaningful signals faster, and positive data often attracts partnership interest. Rare disease is a consistent catalyst category because smaller trials can reach endpoints faster, orphan incentives can support pricing, and the regulatory path can be more structured when disease burden is high and options are limited.

Immunology and inflammation remain attractive because large markets are still shifting toward more targeted mechanisms and better safety profiles, which can open a door for a micro-cap with clean data. Neurology and mental health are especially watchable in 2026 because trial design and regulatory acceptance are becoming more standardized for certain indications, and there is a growing investor appetite for differentiated therapies with clear real-world demand. Across all these areas, the common thread is the same: the market rewards clean clinical readouts that reduce uncertainty, expand probability-adjusted value, and make “next steps” obvious.

Why Balance Sheet and Trial Design Matter More Than Hype in Micro-Cap Biotech

The micro-cap biotech world is not only about scientific potential—it’s also about survival and execution. Even strong clinical data can be muted if a company lacks cash runway, needs highly dilutive financing, or faces trial design questions that make results hard to interpret. Investors increasingly look at practical filters: Does the company have enough cash to reach the next major clinical catalyst? Are endpoints clinically meaningful and aligned with prior regulatory precedents? Is the patient population well-defined? Are results likely to be interpretable even if they’re mixed?

This is the hidden reason why “major clinical catalysts” can be more powerful than general pipeline updates. A defined catalyst forces a company to show its work. It also forces the market to decide whether the science is real, whether management can execute, and whether the regulatory strategy is credible. In a sector where sentiment can swing quickly, the best setups are often companies where the next milestone is not just “news,” but an actual decision point.

Why 2026 Could Be a Breakout Year for Biotech Micro-Caps

Biotech tends to move in waves. When broader markets are cautious, micro-cap biotech stocks can get ignored, and valuations compress even for credible pipelines. But when catalyst seasons hit—especially when multiple companies report strong data close together—capital rotates back into the sector because investors remember that biotech is one of the few places where a company can create massive value without needing years of economic expansion. In 2026, with a heavy lineup of Phase 2 and Phase 3 readouts, FDA action dates, and clinical trial milestones, the sector has the raw material for that kind of rotation, particularly in under-$5B names where reratings can be dramatic.

This is exactly the environment where a watchlist like “Top 5 Best Biotech Micro-Caps With Major Clinical Catalysts in 2026” becomes practical rather than promotional. The goal isn’t to predict every outcome—it’s to identify where the calendar forces clarity. That includes examples like Achieve Life Sciences, Inc., Avalo Therapeutics, Inc., Moleculin Biotech, Inc., DBV Technologies S.A., and Mind Medicine (MindMed) Inc.—not because the list is about any single name, but because these are the kinds of micro-caps where a single 2026 clinical catalyst can dominate the narrative.

The Core Idea Behind This List: Catalyst Clarity, Not Guesswork

At its core, this article is built around a simple biotech reality: timelines move prices. When the market knows a Phase 2 readout is coming, it starts repricing risk. When Phase 3 topline data hits, it reprices the entire revenue possibility. When an U.S. Food and Drug Administration decision arrives, it can instantly redefine the investment case. That’s why “biotech clinical catalysts 2026,” “biotech micro-cap stocks,” “FDA approval,” “PDUFA date,” “Phase 3 trial results,” and “topline data” aren’t just keywords—they’re the vocabulary of how value is created and destroyed in biotech.

And that’s the sector backdrop for 2026: a year where clinical proof, regulatory milestones, and execution discipline are likely to matter more than vibes, narratives, or general market hope—making biotech micro-caps one of the most catalyst-driven hunting grounds in public markets.

CHECK THIS OUT: Why Crinetics Pharmaceuticals (CRNX) Is the “Slow Burn” Biotech Investors Love and Lexicon Pharmaceuticals (LXRX) Proves That Boring Science Can Still Move Markets.

Our Methodology

Our ranking for Top 5 Best Biotech Micro-Caps With Major Clinical Catalysts in 2026 started with a screen of biotech stocks listed on the NYSE or NASDAQ, filtered to companies with market caps below $2 billion, then narrowed to those with clearly defined 2026 catalysts (FDA decision timelines, NDA/BLA-related events, or Phase 2/Phase 3 topline readouts). We ranked the final five from greatest to least market cap to keep the list consistent and investable, while also weighing catalyst strength and timing (how close and how meaningful the event is), pipeline focus and probability of success signals (trial stage, endpoints, and clinical context), balance sheet and cash runway (ability to reach the catalyst without heavy dilution), recent execution and guidance credibility, and valuation/liquidity factors (trading volume and volatility) to avoid purely hype-driven picks.

Top 1: Moleculin Biotech Inc. (NASDAQ:MBRX)

Market cap: $0.01 billion

Moleculin Biotech sits in the part of the market most investors love to hate: a micro-cap biotech stock with a history of volatility, dilution risk, and a share structure that has required corporate actions like a reverse stock split to stay compliant. The company effected a 1-for-25 reverse stock split that became effective December 1, 2025, explicitly consolidating shares to maintain its Nasdaq listing. That reality turns many investors off instantly, and honestly, it should raise your standards. But here’s the twist that creates the bullish thesis: when the market avoids a name for structural reasons, the valuation can become disconnected from the actual scientific and clinical progress inside the pipeline. In micro-cap biotech, that disconnect is often where the biggest upside lives, because the “price” is driven by sentiment and financing fear, while the “value” is driven by clinical milestones.

The bull case for Moleculin is not that risk disappears. The bull case is that the company has a late-stage flagship program with multiple near-term catalysts, a credible attempt to solve one of oncology’s ugliest tradeoffs, and enough pipeline optionality to create multiple shots on goal. If even one of those programs proves out clinically, the re-rating can be violent precisely because expectations are low and the float tends to be reactive. That’s the micro-cap biotech setup in a single sentence: asymmetric outcomes, where most of the time you get nothing, but when you get something real, it moves the entire market cap.

For SEO and search intent, it’s also worth being direct about what people are actually looking up: Moleculin Biotech stock, MBRX stock, NASDAQ MBRX news, penny stock biotech catalysts, acute myeloid leukemia treatment pipeline, Phase 3 AML trial, FDA Fast Track, Orphan Drug Designation, glioblastoma multiforme drug development, pancreatic cancer clinical trial, STAT3 inhibitor oncology, and non-cardiotoxic anthracycline. This thesis is built around those exact demand drivers, because the company’s story is fundamentally about high-unmet-need oncology indications and the kind of trial milestones that can change sentiment overnight.

What Moleculin Is Really Building: A “Next-Generation Anthracycline” Thesis, Not a One-Press-Release Story

Moleculin’s core narrative centers on Annamycin, also referred to as naxtarubicin, which the company positions as a “next-generation” anthracycline designed to avoid key resistance mechanisms and, critically, to avoid the cardiotoxicity that limits traditional anthracyclines. This framing matters because it targets a structural pain point in cancer therapy: oncologists often rely on highly effective drug classes that carry cumulative toxicity ceilings. If you can preserve the efficacy while reducing the long-term organ damage, you’re not just creating another oncology drug—you’re potentially reshaping where and how a whole class of medicines can be used.

The company has been consistent about pushing this idea beyond a single indication. In addition to relapsed or refractory acute myeloid leukemia (AML), it has described development efforts and/or clinical interests in soft tissue sarcoma lung metastases and broader investigator-initiated exploration in other difficult tumors. When you see a company repeatedly expanding the “where this could work” map, you should be skeptical by default. But in this case, the expansion is tied to a specific mechanistic claim: Annamycin’s tolerability profile, especially around the heart, could allow higher cumulative exposure than standard anthracyclines, while its design may help address drug resistance that cripples outcomes in heavily pre-treated patients.

That is the heart of the bullish thesis: Annamycin is not being sold as a marginal improvement; it’s being positioned as a step-change candidate in a class where step-changes could unlock meaningful commercial value.

The Big Catalyst Engine: The Phase 2B/3 MIRACLE Trial in Relapsed or Refractory AML

If you want the cleanest “why now” for Moleculin Biotech, it’s the MIRACLE trial, described as a pivotal, adaptive Phase 3 study evaluating Annamycin in combination with cytarabine (often referenced as Ara-C), a combination the company calls AnnAraC, for relapsed or refractory AML. In biotech investing terms, this is where a story either graduates into credibility or gets reset. Phase 3 is the arena where the market demands outcomes, not narratives.

What makes MIRACLE particularly important is that Moleculin has been explicit about near-term readouts and trial mechanics. The company has described an initial unblinding expected in Q1 2026 and has also discussed the role of two data readouts in setting the course for efficacy versus control and dose selection for later trial components. That kind of language signals that management is leaning on a design where interim signals inform the path forward, which can compress the timeline for decision-making and market repricing. It does not guarantee success, but it does create defined catalyst windows, and catalysts are what move micro-cap biotech stocks.

Moleculin also described the MIRACLE trial footprint as global, and in its January 2026 outlook it referenced that the global trial spans nine countries. The broader point here is not geography for its own sake; it’s that the company is trying to run a real pivotal program, not a niche academic experiment. That matters when investors evaluate whether a company is capable of generating registrational-quality data.

If you’re searching for MBRX stock catalysts, the MIRACLE unblinding timeline and the planned patient progress markers are the center of gravity.

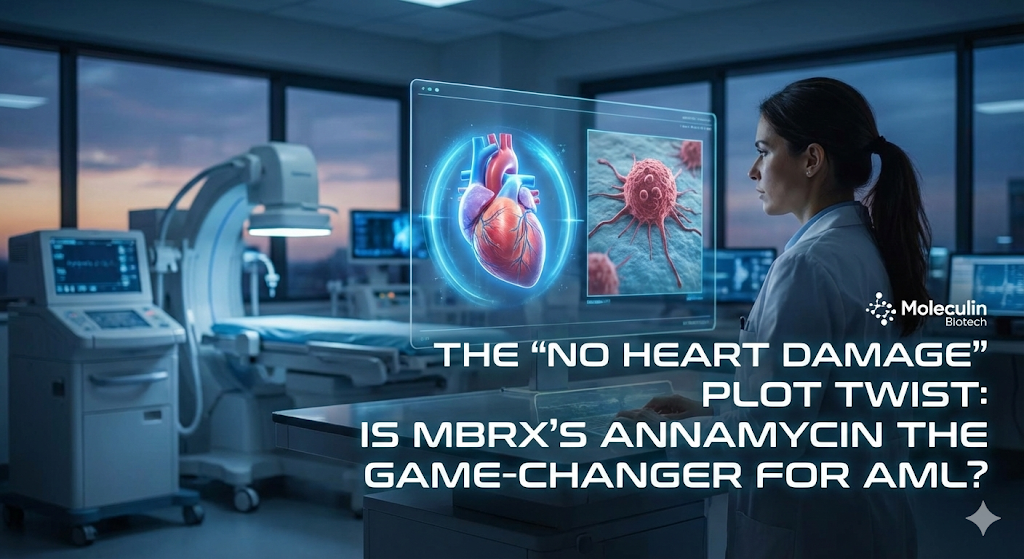

The Differentiator That Could Actually Matter: The “No Cardiotoxicity” Data Narrative

Most small biotech companies can tell you their drug “works in mice.” Very few can credibly argue they’ve addressed a widely known, clinically limiting toxicity that affects huge swaths of oncology treatment. Moleculin has leaned heavily into a claim that Annamycin shows no evidence of cardiotoxicity across a growing dataset. In a January 13, 2026 release, the company said an independent assessment found no evidence of cardiotoxicity across 90 Annamycin-treated subjects reviewed by an expert affiliated with a leading cancer research institute, spanning five clinical trials in AML and soft tissue sarcoma, including both monotherapy and combination with cytarabine. The company described cardiac monitoring methods including serial ECGs, echocardiography with strain analysis, and cardiac biomarkers such as troponins, and it highlighted that many subjects were treated above traditional lifetime cumulative anthracycline exposure thresholds.

That’s a big claim, and it deserves disciplined interpretation. “No evidence” in this context is not the same as “proven safe forever,” and long-term follow-up still matters. Moleculin itself noted the importance of ongoing follow-up and the forward-looking nature of these statements. But as a bullish pillar, this is the type of safety story that can change the conversation, because cardiotoxicity is not a minor side effect; it’s a hard ceiling that can dictate whether patients can receive enough drug exposure to achieve a response, and it’s a long-term survivorship issue in oncology.

If Annamycin eventually shows meaningful efficacy in AML or other settings while maintaining a materially better cardiac safety profile than legacy anthracyclines, the commercial implication is bigger than one indication. It becomes a platform-like oncology asset, with the potential for broader label and lifecycle expansion. That’s why this safety narrative is not just “nice to have.” It’s central to the company’s attempt to create an asset that commands strategic value.

Early Efficacy Signals and the Real-World AML Problem: Resistance and Survival

In relapsed or refractory AML, the market does not reward “interesting biology.” It rewards survival and response in populations that have already failed prior therapies. Moleculin has previously highlighted overall survival signals from its Phase 1B/2 MB-106 study of AnnAraC in AML, including preliminary median overall survival figures in subsets of patients. Again, these are not Phase 3 outcomes, and early-stage data can be noisy, especially in small cohorts. But the bullish interpretation is straightforward.

READ ALSO: Here’s Why Apogee Therapeutics (APGE) Is Suddenly on the Radar of Biotech Investors and Coeptis Therapeutics (COEP) Is Not Profitable Yet — and That’s Exactly Why It’s Interesting.

Disclosure: No relevant interests to disclose. This article was originally published on BioTech HealthX.