We recently published our article Top 10 Cancer Biotech Small-Caps That Could Shock the Market Next. This piece looks at Iovance Biotherapeutics Inc. (NASDAQ:IOVA) as cancer biotech sentiment firms on renewed risk appetite and investors refocus on differentiated pipelines with meaningful upcoming catalysts that can change the company’s trajectory fast.

Cancer biotech has a funny habit: it can go quiet for months, then hijack the entire market in a single morning with one line of text—“met primary endpoint.” That’s not hype, that’s the business model. Oncology drug development is built around proof, and Wall Street prices proof with the emotional range of a weather app in a hurricane. One clean dataset can turn a forgotten small-cap biotech into the most talked-about ticker on NASDAQ or New York Stock Exchange, and one messy readout can erase a year of optimism before lunch. If you’ve been around the biotech tape long enough, you learn this simple rule: in cancer biotech, the calendar matters as much as the science. The real “earnings season” is often the stretch of Phase 2 results, Phase 3 topline data, and regulatory milestones that force investors to stop guessing and start pricing probabilities.

The Odd Trivia That Explains Why Small-Cap Oncology Stocks Move So Violently

Here’s a piece of trivia most people don’t think about until they’re staring at a biotech chart: cancer is not one disease, and “oncology” isn’t one market. It’s dozens of battlefields—solid tumors and hematologic malignancies, first-line and refractory settings, biomarker-defined subgroups, combination regimens, maintenance therapy, and the never-ending chess match of resistance. That complexity is exactly why oncology biotech stocks keep producing surprise winners. A therapy doesn’t need to cure everything; it needs to work clearly in the right slice of patients, with the right dosing, and the right safety profile. When that happens, the commercial runway can be real even if the initial indication is narrow, because success in one tumor type can open doors to label expansion, combinations, and adjacent indications.

Small-cap cancer biotech companies amplify this effect because their valuation is often concentrated in one or two core programs. That concentration is what investors mean when they talk about “asymmetric upside” in biotech stocks. A multi-billion-dollar pharma can absorb a failed trial. A small-cap oncology developer often can’t—and that’s precisely why it can shock the market next if the data lands the right way. The move isn’t just about revenue forecasts; it’s about probability rerating. The market goes from “maybe” to “measurable,” and the stock reprices like it’s waking up in a different universe.

Why “Clinical Catalysts” Are the Real Currency in Biotech Investing

In normal industries, investors obsess over sales cycles, margins, and guidance. In clinical-stage biotech, especially oncology, the language is different: primary endpoint, hazard ratio, durability of response, safety/tolerability, response rate, progression-free survival, overall survival, and whether the trial design matches what regulators and clinicians actually respect. That’s why biotech investors sound like part-time statisticians. A “major clinical catalyst” isn’t just news—it’s an evidence drop that changes the odds.

And yes, the U.S. Food and Drug Administration has a starring role in this drama. FDA approval, accelerated approval discussions, and PDUFA-style timelines are the moments when the market stops debating narrative and starts debating outcomes. If you’re trying to rank cancer biotech small-caps that could shock the market next, you’re really ranking schedules of truth: imminent trial readouts, regulatory decisions, and conference-driven data presentations that force the market to take a side.

The Not-So-Secret Reason These Names Can “Shock the Market”

Another trivia point that separates casual biotech watchers from seasoned ones: in oncology, “good enough” can be transformative. A drug doesn’t have to be perfect to win. It has to be meaningfully better than existing options in a setting where doctors are hungry for something that actually moves the needle. That’s why targeted therapy, precision oncology, antibody-drug conjugates, immunotherapy combinations, cell therapy, and next-generation oncology platforms keep producing these abrupt repricings. The bar isn’t “magic.” The bar is “clinically meaningful,” “statistically credible,” and “commercially adoptable.”

This is where small-cap biotech stocks get their torque. When a company shows a signal that looks reproducible—clean dose-response, consistent benefit across subgroups, manageable safety—investors don’t just model one indication. They start modeling the platform’s right to exist. And that’s when a market cap that looked tiny yesterday starts to look “wrong,” because the addressable opportunity suddenly feels larger and closer.

The Balance Sheet Angle Most People Miss Until It Matters

There’s a reason serious biotech investors keep one eye on the science and the other on the balance sheet. Oncology trials are expensive, timelines are unforgiving, and the market has zero mercy for companies that run out of cash right before a catalyst. So when we talk about “leverage” in small-cap cancer biotech, we’re not talking about debt-fueled financial engineering. We’re talking about runway. Cash runway. Optionality. The ability to reach the next readout without financing panic.

That’s why concepts like market cap, enterprise value, and net cash matter in this list. A company with a relatively low enterprise value versus market cap often has a bigger net-cash cushion, which can reduce near-term dilution risk and give management more flexibility to execute. It doesn’t guarantee success—nothing in cancer drug development does—but it changes the risk profile in a way that the market often rewards when catalysts approach.

What This Article Is Really About

This article isn’t pretending to predict the future with certainty—biotech doesn’t reward that kind of arrogance. What it does is map where the next shocks can come from in the cancer biotech landscape by focusing on small-cap oncology stocks with the kind of setups that historically create violent repricings: meaningful clinical catalysts, credible trial design, real shots on goal, and balance-sheet survivability. The companies on this watchlist sit in that sweet spot where expectations are still fragile enough to be surprised, but the catalyst calendar is loud enough to force a verdict.

If you’ve ever watched a biotech stock triple on a random Tuesday and wondered how anyone saw it coming, the answer is usually boring: somebody was tracking the timeline, the endpoints, the cash runway, and the odds—and they understood that in oncology, the market doesn’t move on vibes. It moves on data.

The Keywords Investors Keep Searching—Because They’re Actually the Rules of the Game

If you’re researching cancer biotech stocks to watch, oncology biotech small-caps, clinical-stage biotech companies, biotech catalysts, Phase 2 results, Phase 3 topline data, FDA approval risk, PDUFA timelines, immunotherapy stocks, targeted therapy, precision oncology, antibody-drug conjugates, CAR-T competitors, and biotech market cap rankings, you’re already speaking the language of how these stocks reprice. This introduction is built around the same reality: in 2026, the biggest market surprises often won’t come from the safest companies—they’ll come from the small-cap cancer biotech names where one dataset can flip the entire narrative.

CHECK THIS OUT: Why Crinetics Pharmaceuticals (CRNX) Is the “Slow Burn” Biotech Investors Love and Lexicon Pharmaceuticals (LXRX) Proves That Boring Science Can Still Move Markets.

Our Methodology

We screened U.S.-listed oncology and cancer-focused biotech stocks on the NYSE and NASDAQ and filtered for small-caps using current market capitalization, then narrowed the universe to companies with identifiable near-term value drivers such as upcoming clinical trial readouts, regulatory milestones, or meaningful program updates that could reprice expectations. We ranked the final ten from lowest to highest market cap for a clean, consistent size-based list, and we sanity-checked each pick using practical “shock potential” signals including enterprise value versus market cap (net-cash optionality), cash runway and dilution risk, liquidity/trading volume, pipeline concentration and trial stage, and the presence of clear catalyst timing rather than vague long-dated promises.

8. Iovance Biotherapeutics Inc. (NASDAQ:IOVA)

Market Cap: $1.00B

Leverage: 24.80%

Iovance Biotherapeutics, Inc. (NASDAQ:IOVA) sits in a rare corner of biotech where the flagship asset is no longer a “maybe someday” clinical promise. The company already has an FDA-approved product on the market, it is actively publishing real-world outcomes, and it is now being judged on the hard stuff that separates legends from footnotes: treatment center expansion, manufacturing throughput, reimbursement flow, physician confidence, and repeatable execution quarter after quarter. In other words, the upside for IOVA stock is no longer driven only by a single trial readout. It’s driven by whether Iovance can scale a complex therapy into a durable revenue engine while pushing the same platform into earlier lines of melanoma and additional solid tumors.

That’s what makes this a compelling bullish thesis setup for investors searching for high-intent terms like Iovance Biotherapeutics stock, IOVA stock analysis, tumor infiltrating lymphocyte therapy, TIL therapy, advanced melanoma treatment, cancer immunotherapy, cell therapy biotech, and biotech catalysts 2026. The market has already seen the first chapter: accelerated approval for lifileucel branded as Amtagvi in melanoma. Now it is watching the next chapters: real-world response rates, a confirmatory pathway, and the commercial ramp that has to prove this isn’t just medically exciting, but economically repeatable.

Amtagvi is not “just another drug”: it’s a one-time, personalized T-cell therapy with a clear niche in advanced melanoma

The core foundation of the bull case is Amtagvi, the first FDA-approved T-cell therapy for a solid tumor indication, approved under accelerated approval for adults with unresectable or metastatic melanoma after anti–PD-1 therapy and, where relevant, targeted therapy for BRAF V600–mutant disease. The approval matters beyond melanoma because it validates a modality that many investors have wanted for years: taking tumor-infiltrating lymphocytes out of the tumor environment, expanding them, and giving them back as a concentrated immune attack. A peer-reviewed FDA approval summary also describes lifileucel as the first tumor-derived T-cell therapy approved, reinforcing that this is a category-creating moment, not just a label update.

Why does that matter for the stock? Because platforms that open new categories often get “multiple shots on goal.” Once a therapy is proven feasible in real clinical practice, the next value drivers become line-of-therapy expansion, new tumor types, and better manufacturing economics. That is exactly the path Iovance is trying to run.

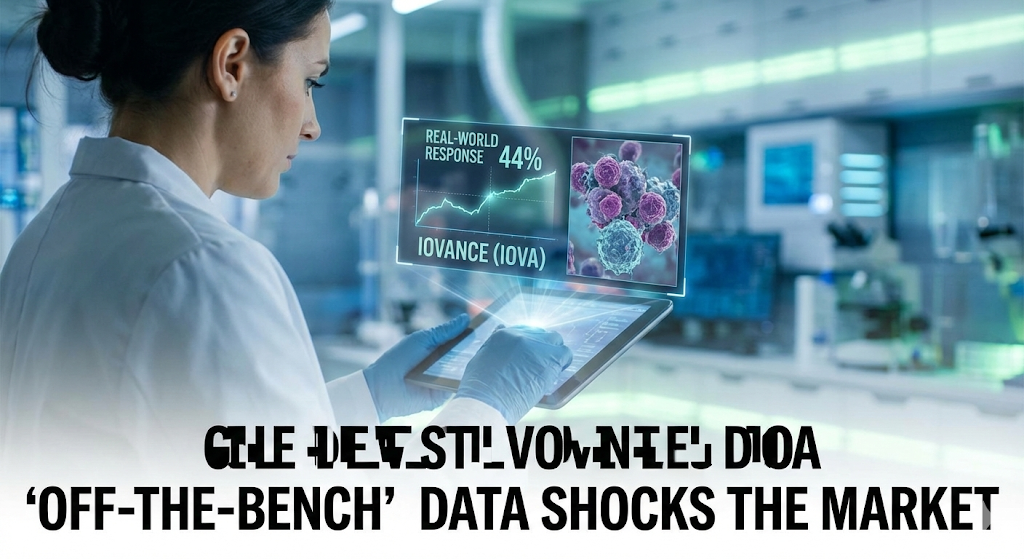

The February 2026 real-world data update is a big deal because it reframes “efficacy” as “repeatable in the wild”

Clinical trials are controlled. Real-world use is chaotic. When a company can show strong real-world outcomes for a high-complexity therapy, it upgrades the story from “interesting in trials” to “working in practice,” and that’s the kind of narrative that can change how institutions model long-term peak sales.

In early February 2026, Iovance released real-world data from four authorized treatment centers in advanced melanoma showing a physician-assessed confirmed objective response rate of 44% (18 of 41 patients) and a disease control rate of 73% (30 of 41). The same update highlighted a key commercial takeaway that investors obsess over: outcomes looked better when used earlier. In patients who received Amtagvi after two or fewer prior lines of therapy, the objective response rate was 52% (12 of 23), versus 33% (6 of 18) after three or more lines.

That “earlier is better” pattern is bullish for two reasons. First, it supports physicians thinking about the therapy sooner rather than as a last-ditch option, which expands addressable patients. Second, it sets up a strategic push into earlier-line settings that could materially change the commercial ceiling if confirmatory evidence aligns. The deeper point here is that commercial medicine is not just about labeling; it’s about how doctors actually choose therapies in the real world, and data that supports earlier use tends to accelerate adoption if the logistical hurdles are manageable.

Accelerated approval creates a clear checklist: confirm the benefit, then widen the runway

Here’s the honest part that actually strengthens the thesis when stated clearly: accelerated approval means continued approval may depend on confirming clinical benefit in a confirmatory trial. This isn’t a weakness; it’s a known checklist. The market can model it. The company can execute against it. And because the therapy is already commercial, each incremental data package can function as both a regulatory support layer and a sales enablement tool.

The February 2026 real-world update itself explicitly compared those outcomes to the 31% objective response rate reported from the pivotal clinical program that supported approval, which strengthens the continuity narrative from trial to real-world practice. When you’re building a long-term IOVA stock bull case, that continuity matters because it reduces the risk that “trial performance disappears once scaled.”

The commercial ramp is the real battleground: revenue guidance, adoption velocity, and treatment center expansion

Iovance’s biggest investor question is not whether the therapy works at all. The question is whether the company can build a predictable commercial machine around a personalized cell therapy, which is harder than selling a pill. That means growth is constrained not only by demand, but also by logistics: how many centers can treat, how fast patients move through referral and scheduling, and how reliably manufacturing delivers product on time.

On the financial side, management reaffirmed full-year 2025 revenue guidance in the range of $250 million to $300 million. For a commercial biotech stock, that matters because it signals the company believes demand plus operational throughput is sufficient to land inside the range, which becomes the base layer for 2026 expectations. At the same time, Iovance’s history in 2025 also shows how sensitive this story is to execution and cost discipline, because scaling a cell therapy launch requires significant spending before the curve fully inflects. When companies adjust headcount or spending plans, it’s often a signal that management is protecting runway while it builds the system needed for durable adoption.

This is where the bullish investor focuses on the right question: not “will sales explode instantly,” but “is the machine getting smoother and more scalable each quarter?” In cell therapy, small operational improvements can have outsized impact, because throughput and cycle-time friction often limit growth more than demand.

Q3 2025 results hinted at operational learning: improving gross margin and a runway into mid-2027

Scaling cell therapy is expensive early and can get more efficient later. So investors watch gross margin as a tell: is the company learning, optimizing, and making each treatment less costly to deliver?

In Q3 2025, Iovance reported total product revenue of roughly $67 million, with the majority from Amtagvi and additional revenue from Proleukin, and it reported gross margin improving to 43%. The company also reported cash resources of roughly $307 million as of September 30, 2025 and stated that this cash position was expected to fund operations into the second quarter of 2027.

That runway matters because the market punishes “great science with no time.” A runway into mid-2027 gives Iovance room to expand treatment centers, streamline manufacturing, and build a referral funnel in the community setting, which tends to be where big numbers come from in oncology. If you’re thinking in SEO terms, this is why searches like IOVA cash runway, Iovance revenue guidance, and Iovance gross margin show up alongside the clinical story: commercialization is a time game, and time is bought with cash.

The platform optionality is the hidden upside: melanoma first, then broader solid tumor expansion

The reason Iovance continues to attract investor attention despite the obvious complexities is that tumor-infiltrating lymphocyte therapy is not limited to one cancer type in principle. The company has long positioned TIL therapy as a platform approach across solid tumors. For long-term investors, this is the “multiple shots on goal” angle: once manufacturing and logistics are industrialized for one indication, marginal expansion becomes easier because you’re scaling an existing system rather than inventing a new one.

This is where the upside can become much larger than the melanoma niche alone. If Iovance can demonstrate that its manufacturing process is reliable, that treatment centers can run the therapy smoothly, and that payers reliably reimburse, then the therapy becomes a template. That template can be applied to additional tumor types and potentially earlier lines of therapy, where patient populations are larger and outcomes can sometimes improve.

Of course, platform optionality only matters if the first commercial program proves durable. But that’s the point: the commercial ramp is the gate that unlocks the broader platform valuation.

The near-term catalyst calendar matters, because biotech stocks move on narrative inflection points

Even when a company is commercial, biotech valuations still respond to discrete events: earnings calls, guidance updates, new real-world data, and regulatory progression. Iovance scheduled its fourth quarter and full-year 2025 financial results and corporate updates for February 24, 2026. That date matters because investors will be looking for three things that can change the stock’s trajectory quickly: confirmation of full-year revenue within guidance, clarity on 2026 demand and treatment center dynamics, and operational indicators that manufacturing throughput and cycle times are improving.

These are the moments when investor interest spikes for terms like IOVA earnings, Iovance 2026 outlook, Amtagvi sales, and biotech catalysts this week. Anchoring the story around real dates and real disclosures is not only good research practice, it’s also how you build organic credibility that ranks well and holds reader attention.

The bear risks are real, but they’re the same risks that create upside if Iovance executes

The first risk is confirmatory risk tied to accelerated approval. Continued approval may depend on verifying clinical benefit, and timelines matter.

The second risk is operational scale. Personalized cell therapy has real-world bottlenecks: center capacity, referral friction, and manufacturing reliability. The flip side is that every operational improvement can expand effective capacity without needing a proportional increase in fixed cost, which is how margin expansion happens in scaling models.

The third risk is commercialization and payer scrutiny. Innovative oncology therapies can face payer pushback, and adoption can vary by center and region. But strong response rates in real-world cohorts, especially the earlier-line response signal, are exactly the kind of evidence that can support physician confidence and payer acceptance over time.

Finally, competition is always looming in oncology. The bullish stance here is not “competition doesn’t exist.” It’s that being first matters in cell therapy workflows. Once centers build processes, train teams, and get comfortable with a therapy’s logistics, inertia can work in the incumbent’s favor—provided outcomes and reliability remain strong.

Bottom line: IOVA is a high-volatility commercial biotech with a real product, improving evidence, and a scaling question the market will keep repricing

If you want the shortest version of the long bull thesis, it’s this: Iovance already cleared the hardest scientific hurdle by earning FDA approval for a first-in-category solid tumor T-cell therapy, and now it’s stacking real-world evidence that suggests the therapy performs strongly in practice, especially when used earlier. The company reaffirmed full-year 2025 revenue guidance of $250 million to $300 million and, as of late 2025, reported cash resources around $307 million with an expected runway into Q2 2027, which buys time for the commercial ramp to mature.

For investors, that makes IOVA stock a pure execution story in 2026: can Iovance turn a complex but powerful therapy into a repeatable commercial system, then use that system to expand into earlier melanoma and broader solid tumors? If the answer is yes, the valuation debate shifts from “can this launch work at all” to “how big can it get,” and that’s where outsized upside typically comes from in differentiated oncology platforms.

READ ALSO: Here’s Why Apogee Therapeutics (APGE) Is Suddenly on the Radar of Biotech Investors and Coeptis Therapeutics (COEP) Is Not Profitable Yet — and That’s Exactly Why It’s Interesting.

Disclosure: No relevant interests to disclose. This article was originally published on BioTech HealthX.